New Framework Balances Actuarial and Solidarity Fairness in Insurance Pricing

Summary

Researchers propose the α-Fair Individual Solvent Premium (α-FISP) framework to address the tension between actuarial and solidarity fairness in insurance pricing. This constrained optimization approach allows decision-makers to select an operating point along a fairness spectrum while guaranteeing solvency.

Why it matters

For insurance professionals and regulators, this framework offers a principled, computable method to address the persistent fairness dilemma in pricing. It enables transparent decision-making, helps navigate regulatory pressures, and can lead to more equitable yet solvent insurance products.

How to implement this in your domain

- 1Evaluate current insurance pricing models against the α-FISP framework to identify potential fairness trade-offs.

- 2Utilize the α-FISP model to quantify and manage cross-subsidization within different risk classes.

- 3Collaborate with actuaries and data scientists to implement the constrained optimization task for premium adjustments.

- 4Engage with regulators to demonstrate how α-FISP can align pricing strategies with state-level fairness requirements.

- 5Develop new insurance products that explicitly leverage the α-FISP continuum to offer customizable fairness options to consumers.

Who benefits

Key takeaways

- Insurance pricing faces a fundamental tension between actuarial and solidarity fairness.

- The α-FISP framework offers a computable solution to balance these two fairness notions.

- It allows for selecting a point on a fairness continuum while ensuring insurer solvency.

- The framework is computationally tractable and aligns with diverse regulatory needs.

Original post by Tianhe Zhang, Xiguang Liu, Peng Shi

"arXiv:2606.14898v1 Announce Type: new Abstract: Fairness in insurance pricing remains a long-standing and deeply debated puzzle. On one hand, insurers, driven by profitability considerations, set premiums that differentiate across individual risks to achieve actuarial fairness. O…"

View on XOriginally posted by Tianhe Zhang, Xiguang Liu, Peng Shi on X · view source

Want to go deeper?

Turn these trends into skills with Learnijoy's hands-on AI & tech courses.

Explore coursesMore in AI Investing

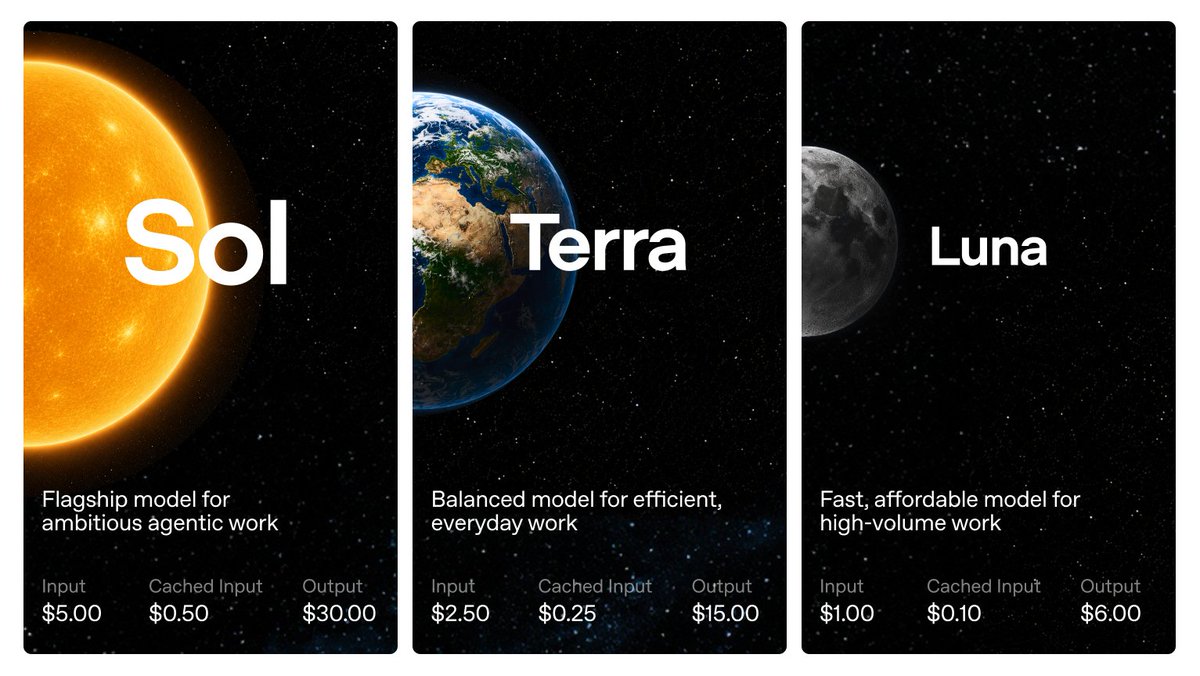

OpenAI's Cryptic Crypto Commentary Sparks Market Speculation

A recent comment suggests OpenAI is engaging in 'trollmaxxing' related to cryptocurrencies like Solana, Terra, and Luna, sparking speculation about its potential involvement in the crypto space.

Public Access to Frontier AI Models May End by 2026

A recent post suggests that public access to the most advanced AI models will cease after 2026, likening these frontier models to nuclear secrets due to their strategic importance.

Apple Raises Product Prices, Citing AI Industry Costs

Apple has increased prices across several products, including MacBooks and iPads, with CEO Tim Cook attributing these hikes to the rising costs driven by the AI industry's demands.