Value Investing Rules Enhance Modern AI for Equity Selection

Summary

This research demonstrates that integrating Benjamin Graham's classical value investing rules with modern machine learning models significantly improves systematic equity selection, leading to higher returns and reduced risk compared to complex AI models alone. The study found that Graham's "margin of safety" effectively prevents AI from taking on excessive risk.

Why it matters

Financial professionals and quantitative analysts can leverage classical value investing principles to build more robust and less volatile AI-driven investment strategies, improving long-term returns and risk management in an increasingly complex market.

How to implement this in your domain

- 1Integrate Graham's principles: Incorporate fundamental value metrics (e.g., P/E, P/B, debt-to-equity) as features in existing machine learning models for stock selection.

- 2Backtest hybrid models: Develop and rigorously backtest investment models that combine traditional value factors with modern quantitative signals across diverse market conditions.

- 3Prioritize risk-adjusted returns: Shift focus from purely maximizing returns to optimizing for risk-adjusted metrics like the Calmar Ratio, using value filters to reduce volatility.

- 4Educate investment teams: Train quantitative and fundamental analysts on the benefits of blending classical investment wisdom with advanced AI techniques.

Who benefits

Key takeaways

- Classical value investing rules can act as a "low-pass filter" for modern AI models.

- Combining Graham's rules with AI improves risk-adjusted returns in equity selection.

- Pure Graham-based models can outperform complex AI models in terms of risk management.

- The "margin of safety" remains a vital concept for preventing excessive AI-driven investment risk.

Original post by Augusto Eiji Yamazaki, Hugo Garrido-Lestache Belinchon

"arXiv:2606.24575v1 Announce Type: new Abstract: Modern finance relies heavily on complex machine learning models to find patterns in the stock market. However, as these AI models get more complicated, they often memorize short-term market noise instead of finding companies with r…"

View on XOriginally posted by Augusto Eiji Yamazaki, Hugo Garrido-Lestache Belinchon on X · view source

Want to go deeper?

Turn these trends into skills with Learnijoy's hands-on AI & tech courses.

Explore coursesMore in AI Investing

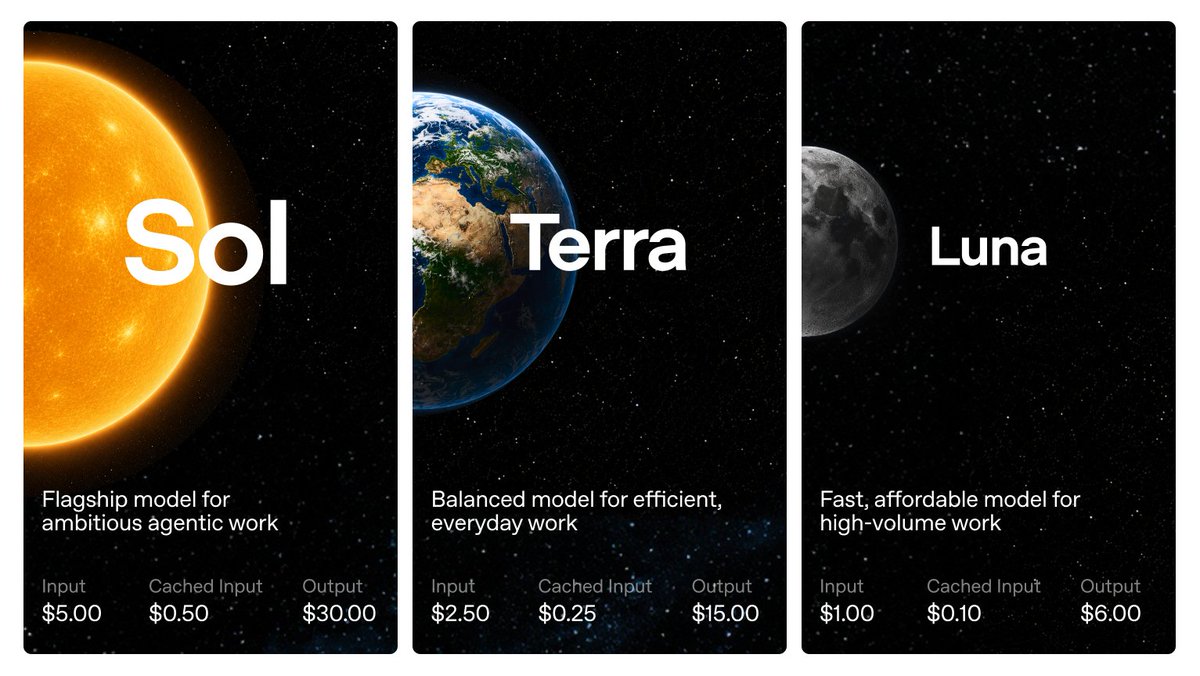

OpenAI's Cryptic Crypto Commentary Sparks Market Speculation

A recent comment suggests OpenAI is engaging in 'trollmaxxing' related to cryptocurrencies like Solana, Terra, and Luna, sparking speculation about its potential involvement in the crypto space.

Public Access to Frontier AI Models May End by 2026

A recent post suggests that public access to the most advanced AI models will cease after 2026, likening these frontier models to nuclear secrets due to their strategic importance.

Apple Raises Product Prices, Citing AI Industry Costs

Apple has increased prices across several products, including MacBooks and iPads, with CEO Tim Cook attributing these hikes to the rising costs driven by the AI industry's demands.